Podcast Center

Podcast Center Video Center

Video Center Webcasts

Webcasts Resource Center

Resource Center Events

Events

By

By  October 08, 2018 at 01:42 PM

October 08, 2018 at 01:42 PM

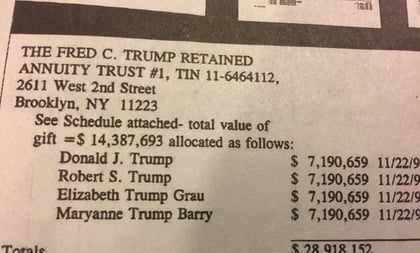

A team of reporters at The New York Times may have given wealth planners something new to talk about with clients, by focusing attention on how the father of President Donald Trump used grantor-retained annuity trusts to transfer wealth.

(Related: Meet the Annuity Trust on Bernie Sanders’ Hit List)

The team has suggested, in a special report package that has been making headlines for a week, that Fred Trump, the president’s father, used a GRAT and other arrangements to transfer assets with a value of more than $1 billion to Donald Trump, and to Donald Trump’s siblings, and to reduce the estate and gift taxes on those transfers to $52.2 million, from a potential tax bill that could have been as high as $550 million.

The reporters themselves note that a lawyer for Donald Trump has said that there was no fraud or tax evasion by anyone, and that the reporters had based false allegations on extremely inaccurate accounts of the facts.

What is a GRAT?

A wealthy individual, or “grantor,” can use a GRAT to convert assets into annuity income.

The grantor puts assets in and takes annuity income out.

When the grantor dies, the beneficiaries can get the value of the assets still in the GRAT without paying estate or gift taxes on those assets.

GRATs and Asset Valuations

A GRAT will perform better if the value of the assets inside the GRAT increases dramatically while the assets are inside the GRAT.