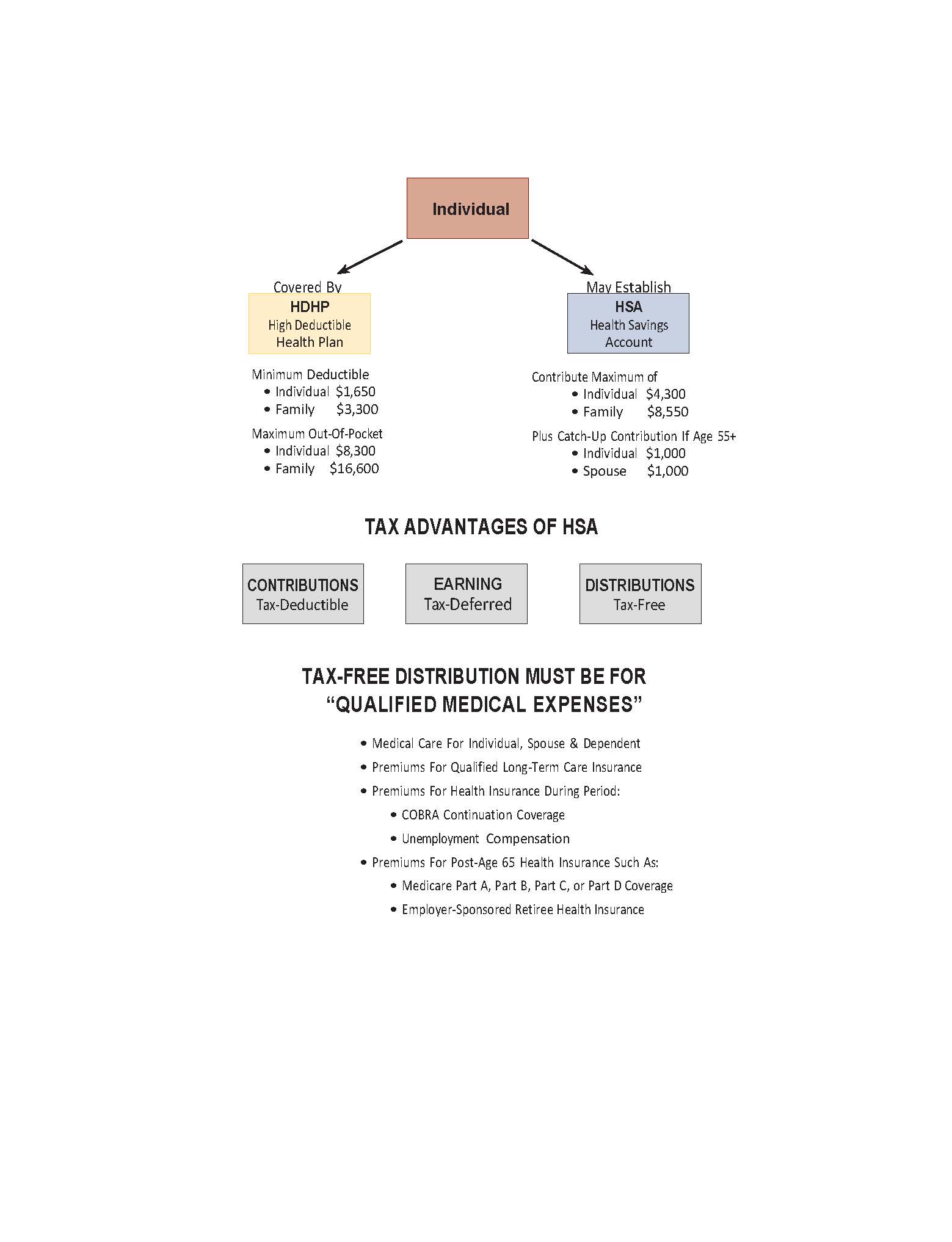

N—Health Savings Accounts

Offering an attractive means of funding future health care costs, a health savings account

(HSA) can be established by eligible individuals covered by a high deductible health plan

(HDHP), provided they are not claimed as a dependent on another person's income tax return

and are not entitled to benefits under Medicare (i.e., have not reached age 65). The 2026

required HDHP must provide for a minimum annual deductible of at least $1,700 for individual

coverage and $3,400 for family coverage; and maximum annual out-of-pocket expenses must

be limited to $8,500 for individual coverage and $17,000 for family coverage. As an exception

to these deductibles, preventive care services may be covered on a first-dollar basis. Annual

contributions to the HSA are limited to a maximum of $4,400 for an individual, or $8,750 for a

family (as adjusted in 2026 for inflation). Account holders and covered spouses, aged 55 and

over, may each make additional contributions of $1,000 in 2026.4 Both the account holders and

their employers can make contributions, but total contributions cannot exceed these annual

limits. Employer contributions for all similarly situated employees must be "comparable" (i.e.,

the same dollar amount or percentage of the annual deductible limit). The account is entirely

owned by the employee. Because unused funds may be carried over from year-to-year, for many

individuals it may be possible to accumulate substantial amounts prior to retirement.

HSAs offer substantial tax advantages. Contributions made by an individual are fully

deductible from income as an "above the line" deduction (i.e., without regard to whether deductions are itemized). Employer contributions are deductible by the employer, are not taxable to the employee, and are not subject to Social Security and federal unemployment taxes. Earnings within the account are tax-deferred. Distributions are tax-free, provided they are for "qualified medical expenses," a term that is broadly construed to include items such as braces and nursing home costs (but not over-the-counter medications or cosmetic surgery). Distributions other than for qualified medical expenses are taxable and subject to a 20-percent-penalty tax.

The 2025 OBBB included two HSA provisions—allowing individuals with high deductible health plans (HDHPs) to enroll in direct primary care arrangements while remaining HSA eligible as long as the monthly fee does not exceed $150, and expanding the definition of an HDHP to include bronze and catastrophic health insurance plans purchased on the Exchange under the Patient Protection and Affordable Care Act. The bill also permanently extends and makes retroactive the special "telehealth safe harbor" established under the Coronavirus Aid, Relief, and Economic Security (CARES) Act that expired December 31, 2024, for HSA-compatible HDHPs.

Although payments of health insurance premiums are not considered qualified medical expenses, exceptions allow tax-free reimbursements for premiums paid for a qualified long-term care insurance contract, premiums for COBRA continuation coverage, and premiums for healthcare while receiving unemployment compensation. For those who are eligible for Medicare, tax-free distributions can be made for post-age 65 health insurance such as Medicare Parts A, B, C, and D, and employer-sponsored retiree health insurance (but not for a Medicare supplement policy).