M—Health Reimbursement Arrangements

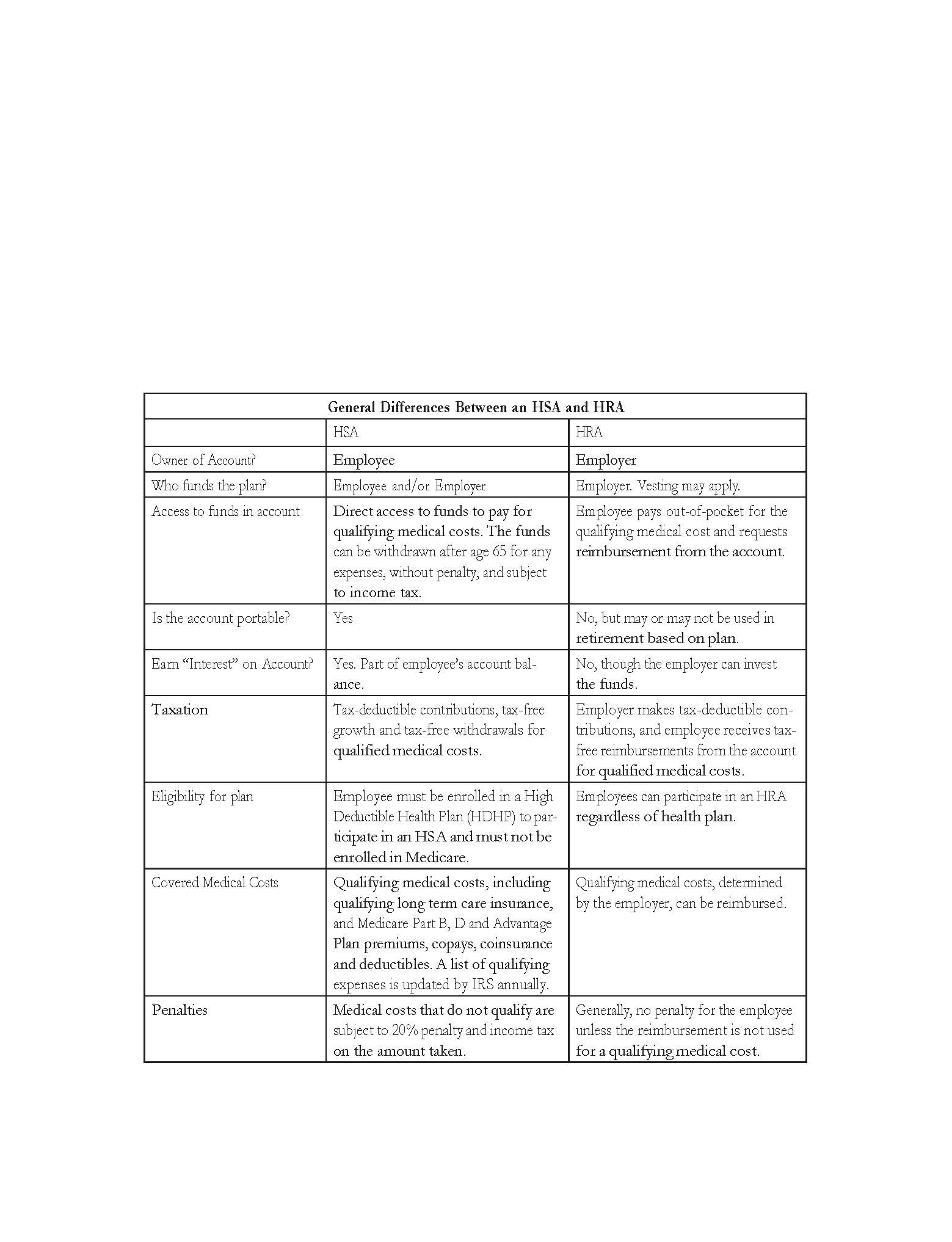

Both a Health Savings Account (HSA) and a Health Reimbursement Account (HRA) can help employees afford out-of-pocket medical expenses on a tax-advantaged basis and can help employers minimize the cost through tax incentives. The chart below summarizes some of the differences between the two types of accounts:

Under a health reimbursement arrangement (HRA), it is possible to pay for the medical

expenses of an employee and the employee's dependents.

The maximum amount that can be contributed to an HRA depends on the specific type of HRA, as follows:

Individual coverage HRA has no maximum contribution limit, allowing employers to set any allowance they choose.

Qualified Small Employer HRA has annual contribution limits set by the IRS, which are $6,350 for individual coverage and $12,850 for family coverage in 2026.

Excepted Benefit HRAs have an annual contribution limit in 2026 of $2,200.

Group Coverage HRAs have no maximum limit.

HRA Rollovers allow unused funds to roll-over to the next year, up to an annual limit.

MEDICAL EXPENSES include items such as doctor bills, dentist bills, hospital bills, transportation, prescription drugs, dentures, nursing services, eyeglasses, and hearing aids. The ideal plan has the cost of the benefit tax deductible to the employer and not includable in the employee's income.