K—Disability Planning

No estate or financial plan can be considered complete unless there has been an evaluation of the risks of disability.Planning to liveis as important asplanning to die, and the risk is greater.

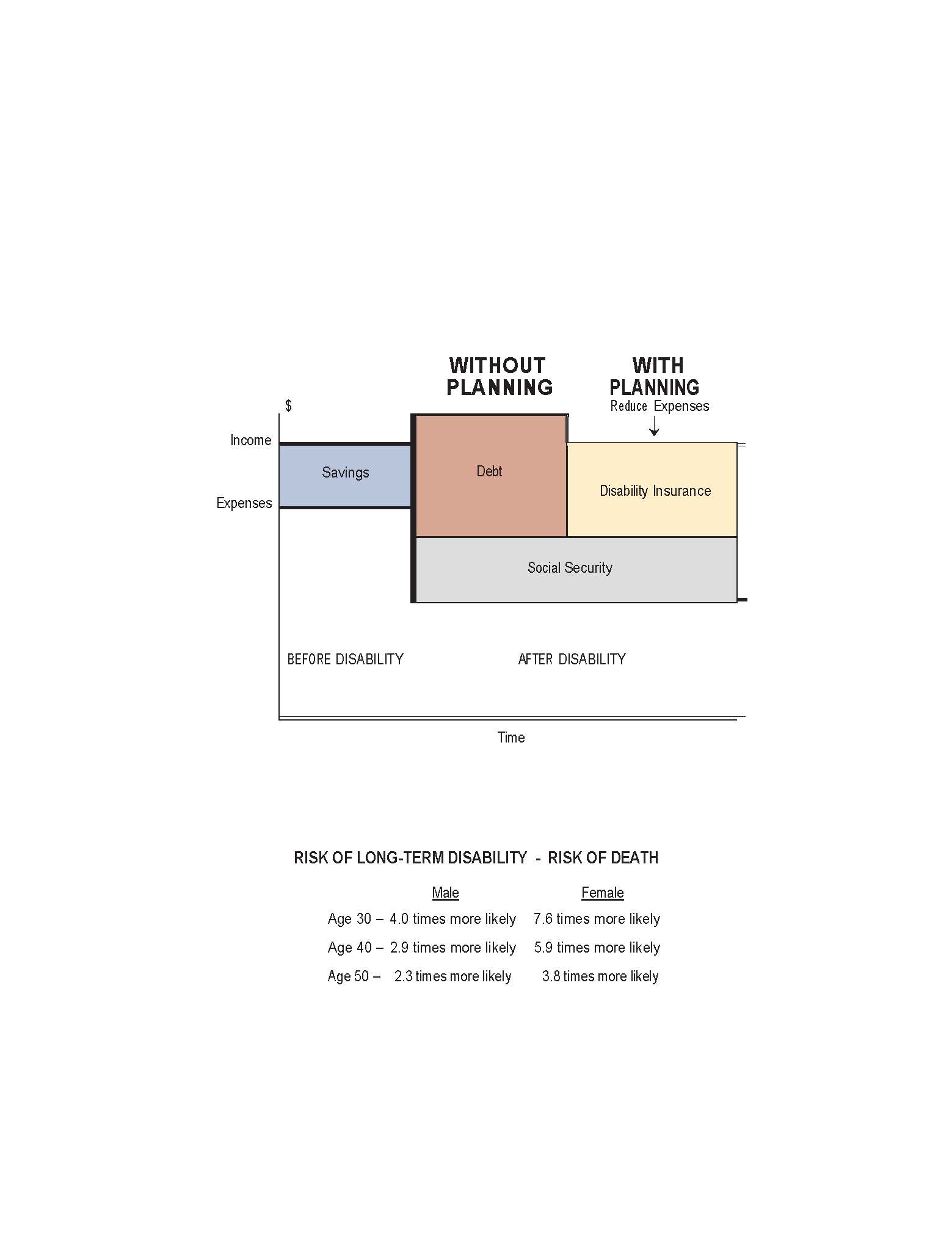

Before disability, most people are able to acquire savings to the extent income exceeds expenses. However,after disabilitycaused by a sickness or injury, income willfalland expenses willrise.

WITHOUT PLANNING,the expenses of a disability can quickly exhaust the family's savings and create substantial debt. This is true despite the availability of Social Security after six months of continuous and total disability. For most people these payments will rarely fill the gap created between falling income and increasing expenses. When available, Social Security disability payments to a disabled wage earner with children will be substantially more than those to a disabled wage earner without children. The fact that a disabled wage earner is married – and often responsible for the financial needs of a spouse – does not result in an increase in Social Security payments.

Today, many life insurance contracts can be purchased with riders that also protect against long-term care events or chronic illness. While these hybrid life products are not disability insurance they can provide a lower cost alternative that can protect against some of the same risks.