I—Recapitalization

A recapitalization through a preferred stock redemption can offer an effective and versatile estate planning technique for corporate stockholders. For example, when combined with a subsequent gifting program, it can:

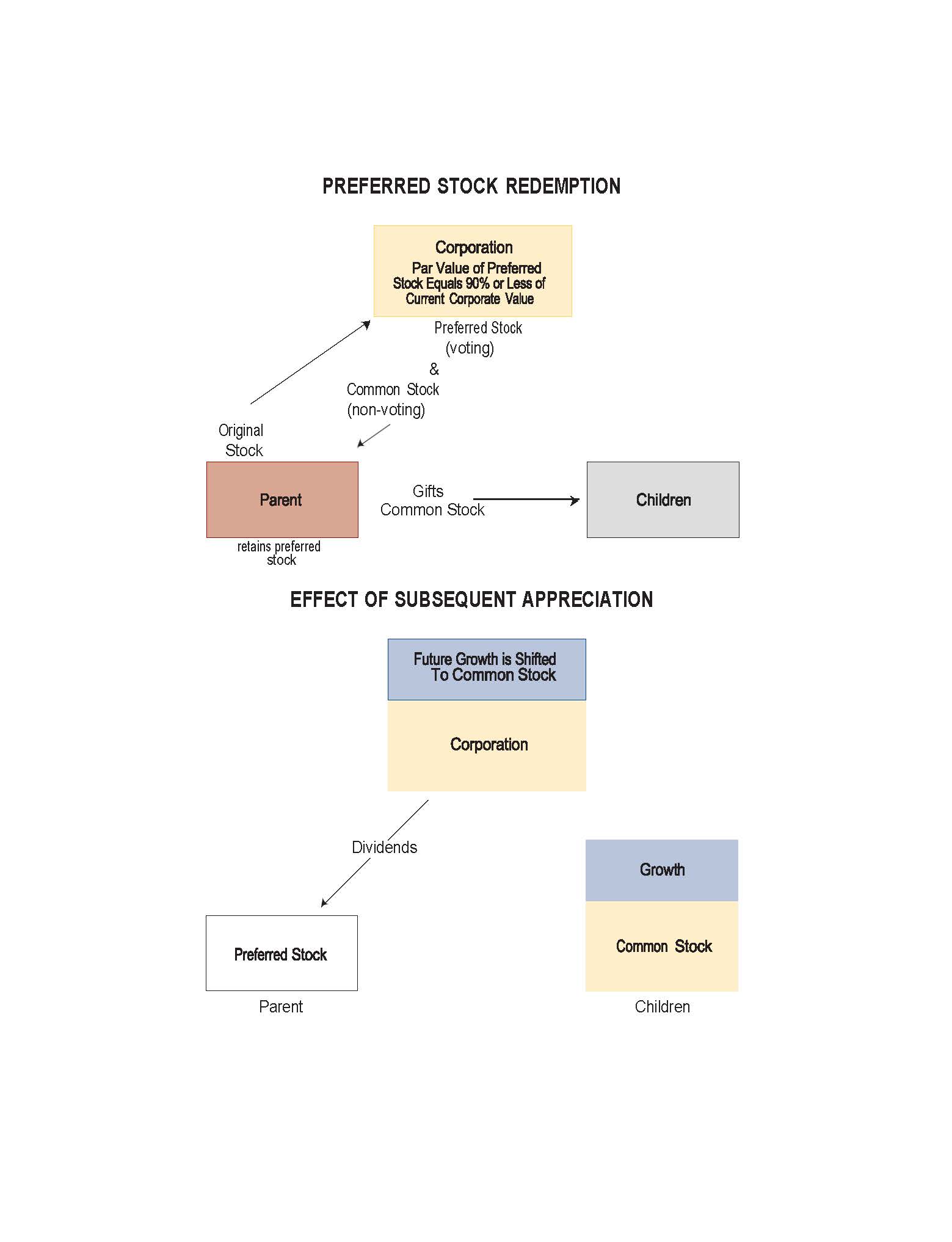

- Shift substantial future appreciation to children.

- Retain control of the corporation.

- Freeze the value of stock for estate tax purposes.

- Provide an ongoing income stream for retirement.

- Transfer corporate control when, and if, appropriate.

- Motivate younger employees.

- Facilitate distribution of stock at death.

The parent retains the voting preferred stock in order to maintain control of the corporation, and the nonvoting common stock is given to the children, or other donees. As long as the retained preferred stock is entitled to dividends, it will be considered to have a value generally equal to the present value of the right to future payments. Because the value of the common stock is determined by subtracting the value of the preferred stock from the total corporate value, the preferred stock's value has the effect of decreasing the value of the common stock, thereby lessening exposure to gift taxes when the common stock is given to the children. However, in order to obtain this increase in value of the retained preferred stock it may be necessary to obligate the corporation to pay substantial cumulative preferred stock dividends.

EFFECT OF SUBSEQUENT APPRECIATION. The prior "freezing" of the value of the preferred stock means that most, if not all, future appreciation is shifted to the common stock owned by the children.

Recapitalizations can be an effective estate planning technique for corporate stockholders who desire to make gifts of stock to children or other heirs. However, they should be undertaken only with the assistance of competent tax counsel.