P—Intentionally Defective Trust

The intentionally defective trust is a wealth-transferring device used by larger estates. It is an irrevocable trust that has been carefully drafted to cause the grantor to be taxed on trust income, yet have trust assets excluded from the grantor's estate. Once established, it can offer multiple planning opportunities and benefits, particularly when combined with both gifts and installment sales.

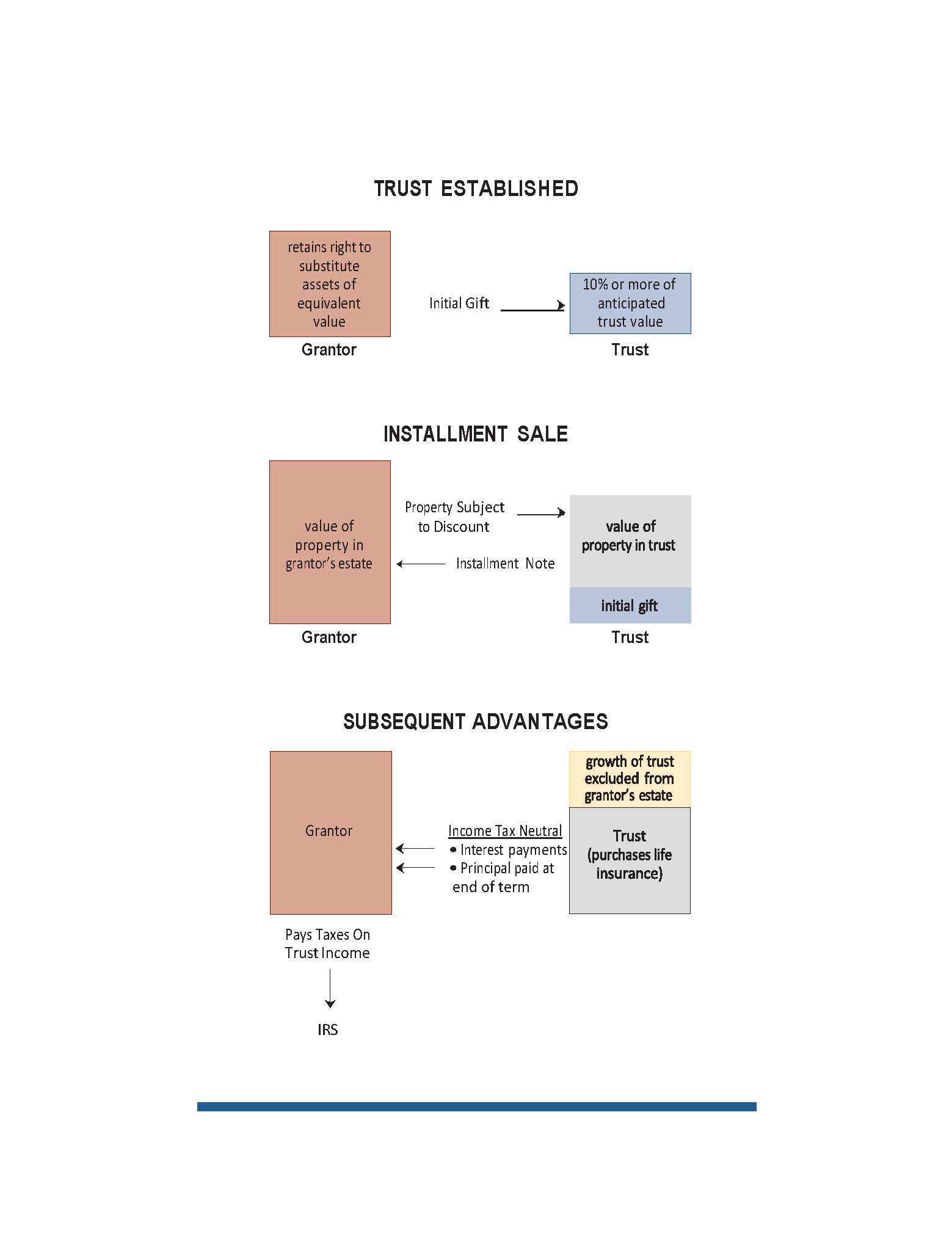

TRUST ESTABLISHED. When establishing the trust, the grantor will typically retain a right to substitute assets of equivalent value. Retention of this right in a nonfiduciary capacity violates one of the grantor trust rules. The grantor is then considered the "owner" of the trust for income tax purposes, but not for estate, gift, and generation-skipping tax purposes. As to income taxes, the grantor and the trust are considered one and the same; trust income, deductions, and credits are passed through to the grantor.

Once established, the grantor then makes a gift of cash or other liquid assets to the trust, equal in value to 10 percent or more of the value of the property that will be sold to the trust in the subsequent installment sale.

INSTALLMENT SALE. Thereafter, the grantor and the trustee enter into a sales agreement providing for the purchase of additional assets from the grantor at fair market value. Under this agreement, the trustee gives the grantor an installment note providing for payment of interest only for a number of years, followed by a balloon payment of principal at the end of the term. The assets sold will typically consist of property subject to a valuation discount (e.g., a non-controlling interest in a limited partnership, a limited liability company, or an S corporation). The amount of this valuation discount is immediately removed from the grantor's estate.

SUBSEQUENT ADVANTAGES. Payment of taxes by the grantor upon the trust income enables the trust to grow income tax-free and is a tax-free gift from the grantor to the trust beneficiaries. The interest and principal payments by the trust are "tax neutral," meaning that they have no income tax consequences for either the grantor or the trust. Any growth of invested trust assets is excluded from the grantor's estate.

If appropriate, the trustee could also use cash flow in excess of required interest payments to purchase life insurance on the grantor. Since the grantor/insured is not the "owner" of the trust for estate tax purposes, the death proceeds would be excluded from the grantor's estate.