B—Life Insurance Products

Below is a list of general life insurance product design categories:

Below is a list of general life insurance product design categories:

TERM INSURANCE. If an estate plan is to be built on a solid foundation, life insurance protection is essential. Term insurance provides protection for a limited period of time. However, the premium for this protection will usually increase, until it becomes prohibitively expensive for most people to maintain. While term insurance can provide a lot of protection for a lesser cost, it builds no cash values and has no permanent values. While some term insurance is "convertible" to permanent coverage and can preserve insurability, it is important to understand the policy details pertaining to conversion because sometimes the ability to convert is limited in time or to certain (undesirable) products in the carrier portfolio.

WHOLE LIFE INSURANCE, in contrast to term insurance, provides for a tax-deferred build-up of cash values over the life of the contract.13 Guaranteed whole life, with cash accumulation capabilities enhanced by recent modifications to IRC 7702, remains the top selling permanent life insurance product in the U.S. This cash value element, combined with level or limited premium increases, means that the death benefit will be available for an unlimited period. While the outlay for permanent insurance, including whole life, is greater than term insurance in the early years, most plans provide for payment of a level premium. Typically, both the cash values and the death benefits are guaranteed, unless they are dependent upon payment of projected dividends.

UNIVERSAL LIFE INSURANCE offers flexible premium payments, an adjustable death benefit, and cash values that are sensitive to current interest rates. Most contracts pay a current interest rate which can be higher than that available in the money market. However, these rates are subject to change and are not guaranteed over the life of the contract. The guaranteed interest rate is usually very modest and will likely result in a lapse of the policy if additional premiums are not paid. Likewise, most universal life policies offer lower current (nonguaranteed) mortality charges, but provided for higher guaranteed mortality charges. Taken together, the lower guaranteed interest rate and higher guaranteed mortality charges represent the "downside risk" of a universal life contract.

EQUITY-INDEXED LIFE INSURANCE is a product that ties the crediting rate to an index, such as the S&P 500. These products offer upside if the equity market increases (these products typically have a cap of 10 or 12 percent) but limit the exposure (usually to a floor of zero or 1 percent). In recent years, sales of Equity Indexed products have been the fastest growing segment of the life insurance market. However, the illustration limitations adopted by AG 49-B has moderately eliminated the sale of equity

indexed products in 2023.

VARIABLE LIFE INSURANCE is similar to universal life insurance, except that the underlying cash values can be invested in an equity portfolio, typically a mutual fund or bonds. The policy owner is usually given the opportunity to redirect his or her investment to another portfolio although some limitations and restrictions may be imposed.

PRIVATE PLACEMENT LIFE INSURANCE is a type of variable life insurance policy which typically differs from traditional variable life insurance by investing cash values in less common (or more exotic) investments. Whereas traditional variable life policies typically offer a suite of mutual fund-like investments - a private placement life insurance contract may include venture capital, REITs, private equity, commodities, and hedge funds. Often times, the investment manager is selected by the policyholder. These types of policies have received considerable attention in recent years with some regulators and legislators questioning the taxation of such policies as life insurance rather than as investments. Speciifically, it has been suggested that many of these arrangements provide too much control to the owner (directly or indirectly) and may fail the investor control restrictions imposed on life insurance products. Private Placement Life Policies are typically unregistered securities and, as such, only available to "accredited investors" with a net worth exceeding $1 million (excluding primary residence) or income of at least $200,000 for each of the two prior years ($300,000 for married couples).

FIRST-TO-DIE LIFE INSURANCE, also known as "joint life insurance," insures two or more lives, and pays a benefit upon the first death. Generally, the premium required for a permanent product is substantially less than those for individual policies on each insured.

Uses for first-to-die life insurance include: (1) income replacement in two wage-earner families (e.g., to pay off mortgage); (2) social security replacement for retirees; (3) estate tax payment to facilitate early transfer of appreciating assets to heirs; (4) key person insurance; (5) funding split-dollar rollout of survivorship life insurance and (6) funding both entity purchase and cross purchase agreements.

When funding a cross purchase agreement it is appropriate to have joint ownership of the contract. With equal ownership interests an appropriate beneficiary designation would be: "surviving insureds, equally." With unequal interests an appropriate designation would be: "surviving insureds as their interests may appear in the cross purchase agreement dated ____."

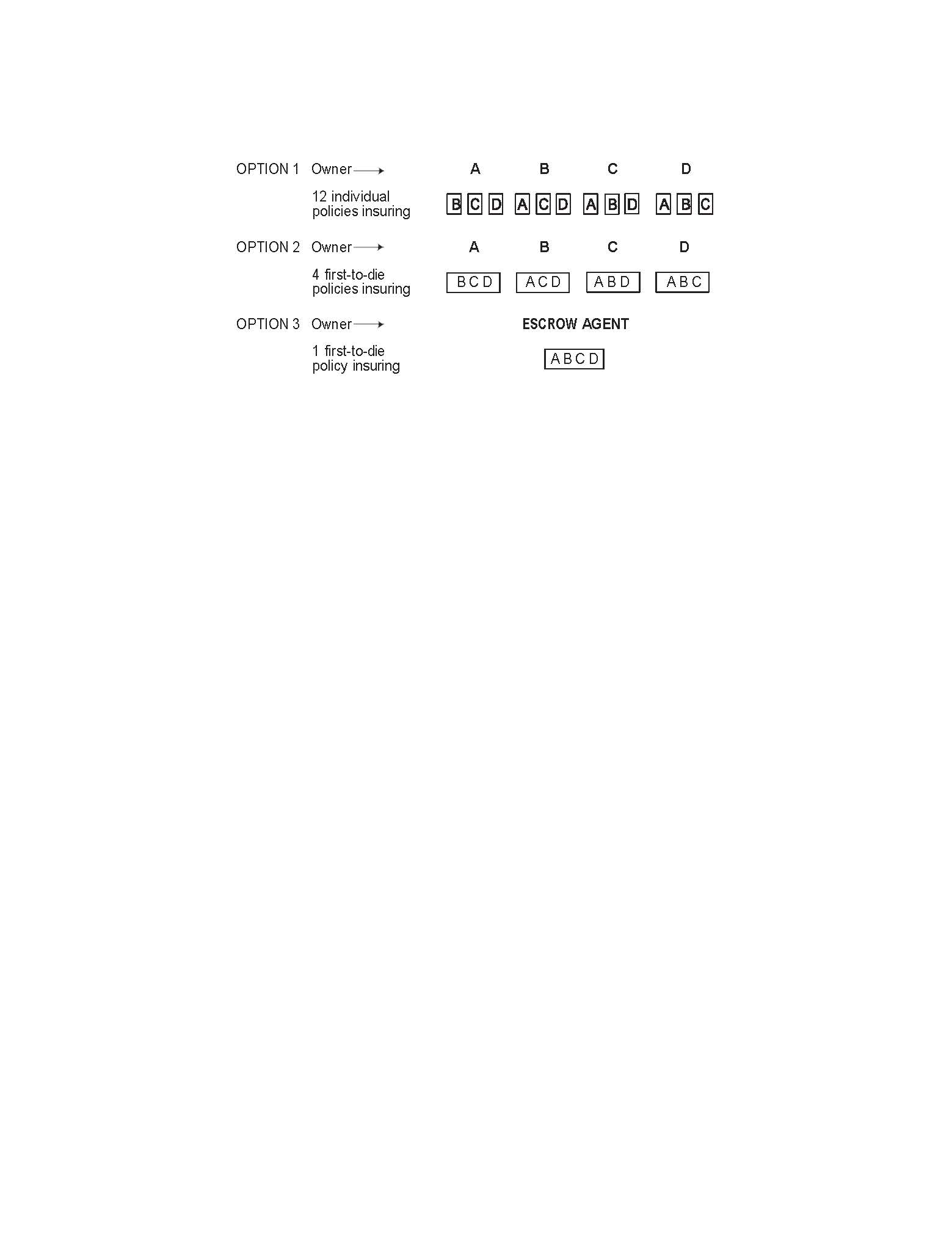

First-to-die life insurance is very effective in reducing the number of policies required to fund multiple-owner cross purchase agreements. For example, funding of a four stockholder cross purchase agreement requires 12 individual policies, but only four first-to-die policies (Options 1 and 2 below). A trusteed cross purchase agreement using an escrow agent requires four individual policies, but only one first-to-die policy (Option 3 that follows). If available, a survivor purchase option provides an effective means of acquiring ongoing insurance for surviving stockholders.

Exercising this option appears to resolve the "transfer for value" problem caused by a transfer of policy interests following the death of a stockholder under a trusteed cross purchase agreement funded with individual policies.

However, first-to-die insurance has not proven to be commercially successful for insurance companies. Because the cost of a first-to-die policy is not always materially less expensive than two individual policies (assuming a two life application), the use of first-to-die product is not as common as might be expected. For this reason, it is increasingly difficult to find life insurance companies that issue this product.

Survivorship life insurance, also known as last-to-die insurance or second-to-die insurance, insures two lives, and pays a death benefit after the death of both insureds. Generally, the premium required is less than that for comparable insurance on either individual life, since the odds of two individuals dying during any given year are substantially less than of one individual dying.

While the many potential uses of survivorship life include charitable gifts, family income for surviving children, and key person insurance. Survivorship life is most often used to fund the payment of estate taxes, when the marital deduction defers taxes until the death of both spouses. Survivorship life offers the advantage of simplicity by paying a death benefit exactly when taxes are due – upon the second death. With a rated or uninsurable client, coverage can usually be obtained, provided the spouse is insurable at standard rates. Despite much higher estate tax exemptions and, therefore, fewer estates subject to estate taxes, second to die insurance has remained popular as a means of leveraging family wealth to leave a significant inheritance upon the second death of mom and dad.

There are some disadvantages to relying solely upon survivorship life insurance to fund the payment of estate taxes. For example, when the marital deduction is used to defer all estate taxes until the second death, appreciation of assets in the surviving spouse's estate can substantially increase total estate taxes. The flexibility provided by the use of disclaimers may be severely limited when there are no funds for payment of estate taxes at the first spouse's death. After divorce the unlimited marital deduction is no longer available, unless the bulk of the estate is left to a new spouse.

Split-dollar is often used to pay premiums on a survivorship policy funding a life insurance trust. The value of the gift to the trust can be substantially reduced by using the very low joint life rates that measure the probability of two deaths in one year. Use of low joint life rates allows substantial coverage to be purchased within the "present interest" limits. But it must be recognized that no death benefit will be paid until both insureds have died. This means that a survivorship policy must generally be funded for longer periods then a policy insuring just one individual. Also, after the first death, the value of the gift to the trust will be measured using higher single life rates. This amount could exceed the $19,000 (as indexed in 2026) annual exclusion limit for present interest gifts.

Equity-Indexed Products (IUL). These are life insurance and annuity products where the crediting rate is tied to the performance of an index (most commonly the S&P 500, but it can involve other indices). These products have been available for some time, but they have become much more popular since late 2010 when the Securities and Exchange Commission withdrew a proposal that might have treated equity indexed annuities as regulated products. That proposal, Rule 151A, was withdrawn after the rule was vacated by the U.S. Court of Appeals for the District of Columbia in July 2010. Under proposed Rule 151A the SEC could have considered an equity indexed annuity a security that would have required selling agents to be equity licensed.

The workings of an EIA can be quite complicated and it is important to fully understand the product. Because they can have so many "moving parts," the following discussion provides, at best, only a general outline of Equity indexed products. Individual contracts can vary greatly from company to company. Second and third generation products are being introduced with new features and new complexities.

Equity indexed products are particularly attractive to individuals who are concerned about the safety of principal but who want the opportunity to experience market related gains. Typically a premium payment is allocated to one or more indices offered by a carrier. Although the premiums are credited to the carrier's general account (as opposed to a variable product with separate accounts).

Insurance companies typically fund indexed products by investing in high grade bonds in order to cover the end-of-term guarantee of principal, pay commissions and make a profit. However, a portion of the remaining funds are used to purchase options (i.e., the right to purchase stock at a fixed price at some future time). If the market goes up selling the call options provides funds for meeting the contract obligations.

The most common index is the S&P 500 for a one-year period. Other indices and time periods (two, three, and five years) are also common. Based on the performance of that index more or less might be credited to the policy owner.

Generally the policy owner will receive credit to their policy based on the performance of the selected index up to a certain cap. For example in a year where the S&P index increased 20 percent, a policy with a 12 percent cap will credit 12 percent to the policy owner's contract.

There are wide variations in how the crediting works with certain contracts offering percentages of the underlying index and other contracts offering no cap, or limit, to the crediting.

The attraction of most indexed products is that there is a floor below which the credit rate cannot fall. This is the most meaningful difference between an equity indexed product and a variable life insurance contract. Typically the floor is zero, although some carriers may offer a slightly higher floor. The attraction is that in a period of time where the selected indices have negative performance (there is a loss below zero) the policy will not be reduced in value. In effect, prior year's crediting is locked in.

In reality there are multiple moving parts to an equity indexed product. For example, carriers may offer high cap rates and, therefore, high illustrated rates. However, there may also be high internal charges within the contract, effectively negating the benefit of a credit received by a high cap rate. A credit to a policy is often not received until the end of the index period (again, often one year). Carriers may charge policy expenses in a variety of ways even before a policy credit is received; this can have an effect on long-term policy performance. Additionally, in years where there is little or no crediting to the policy, internal charges will continue to be assessed on the policy.

Unlike the other methods, this has the effect of locking in gains and annually resetting the starting point of the index. Earnings are typically not credited until the end of the term, thus there is no compounding of interest earned. Averaging can be done daily, monthly, or annually. The usual effect of averaging is to increase the rate in a decreasing market and reduce the rate in a rising market.

A cap (maximum rate) may be set on annual gains in the contract. The participation rate is the percentage of the index movement that will be credited (this can vary widely from 60 to over 100 percent). Some contracts guarantee the participation rate for the term of the contract, while other contracts reserve the right to change the participation rate or even lower the cap.

In effect, equity indexed products offer upside potential with downside protection. However, the long-term performance of these policies remains to be determined. Although numerous carriers show how their indices might have performed based on historic averages, many of these indices did not offer options for much of these periods. As a result true back-testing may not be available.

Moreover, future performance is impossible to predict.