L—Disposition of a Business Interest

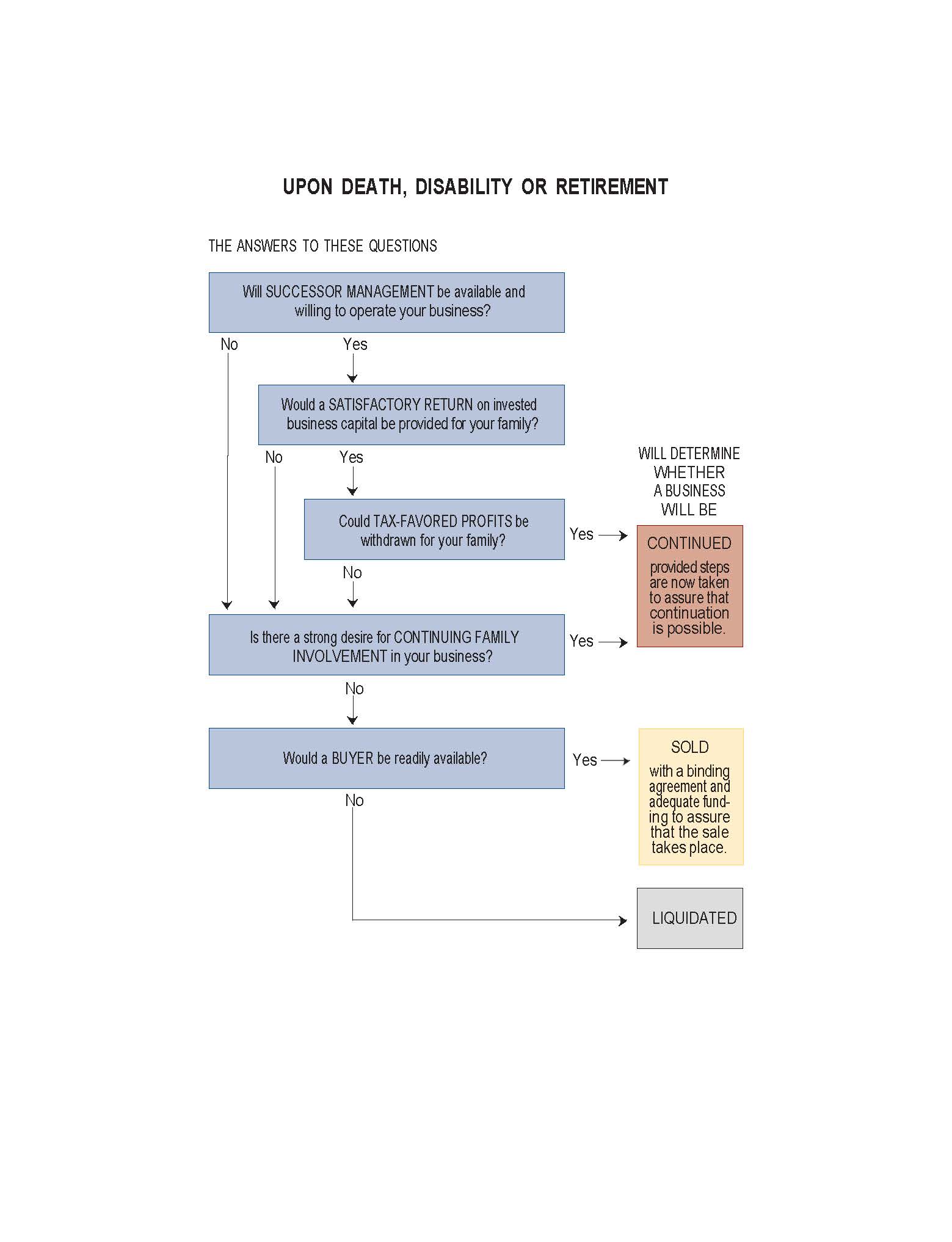

For our purposes, there are three primary risks facing the business owner: death, disability, and retirement. Likewise, upon the occurrence of one of these events, only one of three things can happen to his business: it will be continued, sold, or liquidated. The planning process should reveal the answers to these questions:

Will SUCCESSOR MANAGEMENT be available and willing to operate the business? Such a person could be either a family member or a key employee, but it is important to be realistic about both their abilities and commitment to staying with the business. A yes answer will lead to . . .

Would a SATISFACTORY RETURN on business capital be provided for the family? The decision as to what is "satisfactory" is a highly subjective determination, but it usually falls within the range of 6 to 20 percent.

A yes answer will lead to . . .

Could TAX-FAVORED PROFITS be withdrawn for the family? If the business is a corporation, then payment of a salary to the stockholder-employee is "tax-favored" as a deductible business expense. Under current law, however, the individual shareholder-employee may be in a higher marginal tax rate than the C corporation. Payments to a surviving spouse or non-active shareholder might be characterized as nondeductible dividends.

If the answers to all three of these questions are yes, then it is likely that the business could be successfully continued. However, should the answer to any one of these questions be no, then this would lead to . . .

Is there a strong desire for CONTINUING FAMILY INVOLVEMENT in the business?

A yes answer to this question is often the result of a strong sense of family pride in the business, despite one or more "no" answers to the previous questions. Under such circumstances the business

might well be continued, provided steps are now taken to assure that continuation is possible.

A no answer to this question will lead to . . .

Would a BUYER be readily available? If the answer is yes, then the business should be sold, with a binding agreement and adequate funding in order to assure that the sale takes place. A no answer to this question means that the business is likely to be liquidated and its assets sold for pennies on the dollar.

But, even if all of the above questions can be answered "yes," it's prudent to ask if family wealth and happiness could be maximized by a sale. Just because a family business can be continued doesn't always mean that it should be. Sometimes family wealth, harmony, and happiness is maximized by monetizing the business while the founder is still living and the business is prospering.