Podcast Center

Podcast Center Video Center

Video Center Webcasts

Webcasts Resource Center

Resource Center Events

Events

By

By  March 25, 2024 at 09:29 AM

March 25, 2024 at 09:29 AM

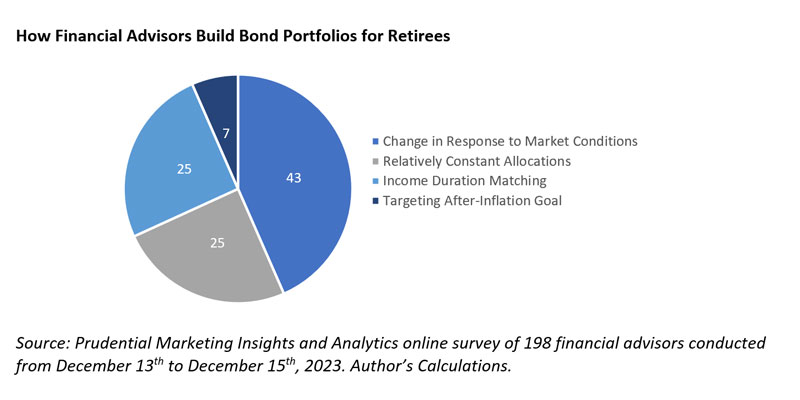

Retirement is the most expensive “purchase” most American households will ever make, with a price tag for many coming in at over $1 million. When it comes to building efficient portfolios for retirees, there are a number of different considerations and perspectives among financial advisors.

To better understand the advisor view, Prudential’s Marketing Insights & Analytics group fielded a survey of 13 questions among 198 financial advisors in December 2023.

Our survey indicates financial advisors, especially those who note expertise in retirement income planning, are clearly interested and focused on building (and using) portfolios specifically designed for retirees. These portfolios often leverage different asset classes than those used in more accumulation-focused strategies.

These results generally suggest advisors increasingly should be aware of the frameworks that exist to develop efficient retirement income portfolios or partner with asset managers that have specific expertise in this domain. Click on the charts below to enlarge.

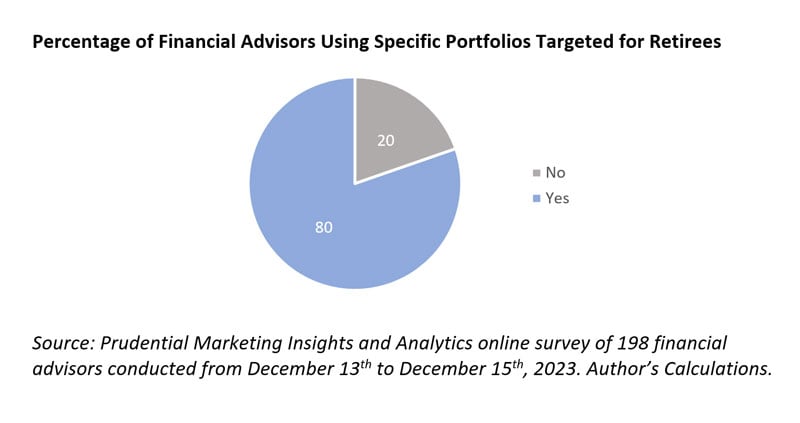

1. Financial advisors use specific portfolios for retirees.

One survey question asked: “Do you build, or use, a separate set of portfolios specifically targeted towards retiree clients?” Eighty percent of respondents said yes.

Use of retiree-specific portfolios was higher among those who were somewhat or very knowledgeable about retirement income planning. In contrast, only 58% of advisors who said they were not very knowledgeable about retirement income planning used retiree-specific portfolios.

This suggests as expertise in retirement income planning increases, these numbers could further increase.

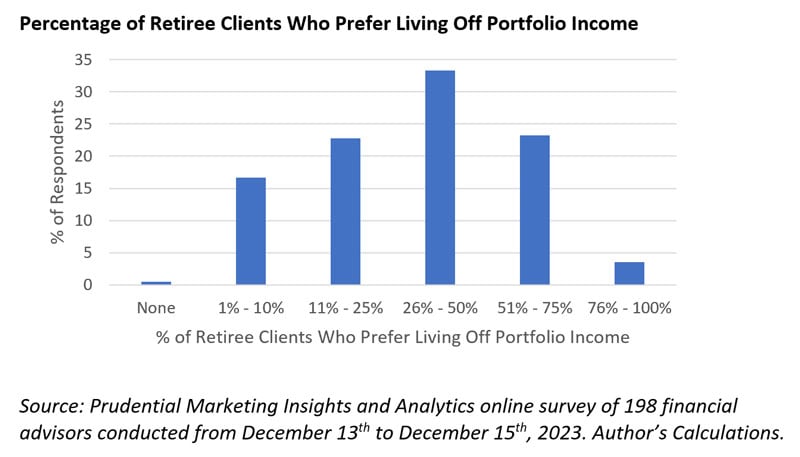

2. Retired clients prefer to live off portfolio income.

Another question asked: “… Approximately what percent of your retiree clients prefer living off portfolio income?” While there is clearly a diversity of responses, overall it appears about 50% of retiree clients prefer to live off of income.

This suggests advisors need to be capable of building portfolios that have an income focus. These portfolios can be very different than the more traditional perspective using mean variance optimization (MVO), which focuses on total return (a combination of income return and price return).

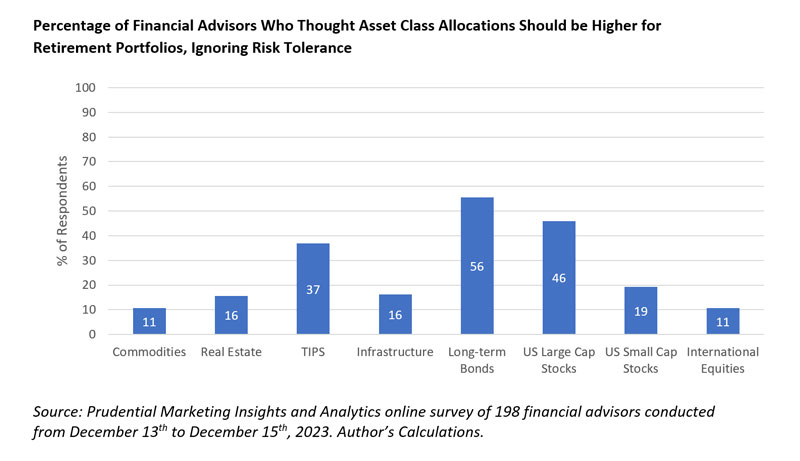

3. Perspectives on using asset classes in retirement portfolios vary notably.

The question asked: “Ignoring risk tolerance, what role do you think the following asset classes should play in portfolios for retirees (versus non-retirees)?”

The graphic includes the percentage of respondents who thought allocations should be somewhat higher or much higher. Financial advisor respondents were most interested in allocation to long-term bonds, U.S. large-cap equities, and Treasury inflation-protected securities.