Podcast Center

Podcast Center Video Center

Video Center Webcasts

Webcasts Resource Center

Resource Center Events

Events

By

By  October 04, 2018 at 03:22 PM

October 04, 2018 at 03:22 PM

Life insurers may be more nervous about taking on income guarantee risk than they used to be, but they have stood up with other financial services companies to urge Americans to seek guaranteed sources of lifetime retirement income.

The 24 companies in the new Alliance for Lifetime Income organized a well-intended press conference in New York today to kick of a major, well-funded lifetime income awareness campaign.

(Related: Companies Form Lifetime Income Outreach Alliance)

The press conference attracted reporters from organizations such as the Wall Street Journal, Bloomberg and Quartz.

The new alliance is a nonprofit, 501(c)(6) business association. The alliance is not promoting any specific product, or type of product. But Barry Stowe, chief executive officer of Jackson, the parent of Jackson National Life Insurance Company, said at the press conference that he believes annuities with lifetime income guarantees can help solve part of a problem that is “hiding in plain sight.”

“We like to think of retirement as the third part of your life, when you get to do what you want,” Stowe said. But, for many Americans, he said, retirement is really about worrying how to make a limited amount of savings last through retirement.

Dennis Glass, the president of Lincoln Financial Group, said life insurers have a unique role to play in meeting lifetime income needs.

“The life insurance industry is the only industry that provides guarantees,” Glass said. “We have to speak louder about the importance [of retirees] protecting a portion of their savings.”

What’s in the Alliance for Lifetime Income awareness campaign?

In addition to the press conference, the campaign itself includes:

- Dubbing Oct. 4 “Protect Your Retirement Income Day.”

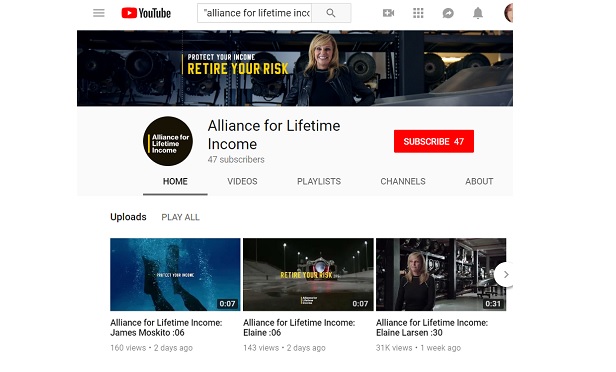

- A national television advertising campaign, with the message, “Retire Your Risk.” Several videos related to the campaign are available here.

- The creation of a new Protected Lifetime Income Index tracking index, which could help draw attention to Americans’ income protection efforts on a regular basis.

- The formation of a group of eight Alliance for Lifetime Income Research Fellows. The list of fellows includes Michael Finke, dean of the American College of Financial Services; Jason Fichtner, the associate director of an international economics and finance master’s program at the Johns Hopkins School of Advanced International Studies; and Seth Harris, a visiting professor at Cornell who, in the past, was the deputy secretary of Labor.

- The opening of a virtual reality booth in New York’s Times Square. In exchange for watching short videos about the importance of protecting retirement income can risk, visitors can use an Oculus headset to enjoy simulated risky situations, in race cars, or at the bottom of the sea. After a day in Times Square, the VR booth will begin traveling to locations all around the country.

What companies are in the Alliance for Lifetime Income?

The Alliance for Lifetime Income came to life in June. The most visible players so far have been insurers, such as Jackson, Prudential Financial Inc. and American International Group Inc.

But the list of alliance founders also includes financial services companies from outside the life insurance sector: Franklin Templeton Investments, Invesco, J.P. Morgan Asset Management, State Street Global Advisors, and T. Rowe Price.

Some insurers have taken pains to send the message that they are part of the alliance. TIAA, for example, put out a press release celebrating Protect Your Retirement Day and pointing out that it helped start the alliance.

Lori Dickerson Fouché, the head of retail and institutional financial services at TIAA, a major annuity provider, said in a statement that TIAA and the other alliance founders see too many people approaching their retirement years without protected retirement income.

“TIAA is thrilled to be able to drive a national conversation on the benefits of annuities in a diversified portfolio,” Fouché said.

Why is the lifetime income issue getting attention now?

Jana Greer, president of the retirement unit at AIG, said giving the issue attention now is critical, because of three “tidal waves” that are sweeping in at the same time: the aging of the U.S. population, increases in the typical retiree’s life expectancy, and the shift to 401(k) plans and other defined contribution retirement plans, from defined benefit pension plans.

Greer said she tried asking five colleagues about their retirement income planning efforts.

“For one thing,” she said, “they haven’t done any of the math.”

Even when people have some idea of what the basic components might be, they usually fail to take inflation into account, she said.

Finke, the American College dean, said another reason for urgency is because so many baby boomers will be retiring without pension income at the same time, without knowing what to do with a retirement nest egg. One common question, he said is, “How do you account for the fact that you don’t know how long you’re going to live?”

Economists know that the solution is pooling retirement assets in a joint arrangement, but many consumers don’t know that, he said.

What obstacles does the alliance face?

One problem alliance must overcome, especially in an age of low interest rates, is that annuities work best for retirees with significant retirement savings.

Only about 20% of U.S. workers say they have $250,000 or more in retirement savings, according to the Employee Benefit Research Institute.

One of the reporters at the press conference said that, if she put $500,000 in one annuity she looked at, she would get just $2,600 in income per month.

Glass said that annuities can help retirees get more out of modest amounts of savings but can’t overcome a failure to save.

Another problem the alliance could run into is the publicly traded life insurers’ quarterly calls with securities analysts. Since the end of the 2007-2009 Great Recession, life insurance company CEOs and chief financial officers have usually spent some time during each call emphasizing the companies’ lack of income guarantee risk, or talking about efforts to reduce income guarantee risk.

Glass said the Great Recession and other downturns show that life insurers have the strength to honor the guarantees they make.

“We’ve weathered the most severe economic periods in the history of the world,” Glass said.

Stowe also defended life insurers’ ability to offer and honor guarantees.

“I think our industry has an enviable track record,” Stowe said.

— Read Jackson Backs New Lifetime Income Alliance With Video, on ThinkAdvisor.

— Connect with ThinkAdvisor Life/Health on LinkedIn and Twitter.

Slideshow

Slideshow