Podcast Center

Podcast Center Video Center

Video Center Webcasts

Webcasts Resource Center

Resource Center Events

Events

December 15, 2017 at 10:22 AM

December 15, 2017 at 10:22 AM

TD Ameritrade recently looked at the challenges of divorce and widowhood in the U.S. and uncovered some disturbing findings.

Sixty-five percent of married individuals do not have a financial plan in place in the event of a divorce or spouse’s death, yet 72% of men and 62% of women expressed confidence in their ability to manage their own financial situation if faced with one of those events.

This comes at a time when some four in 10 marriages fail and about a quarter of Americans 65 and older become widowed, TD Ameritrade said.

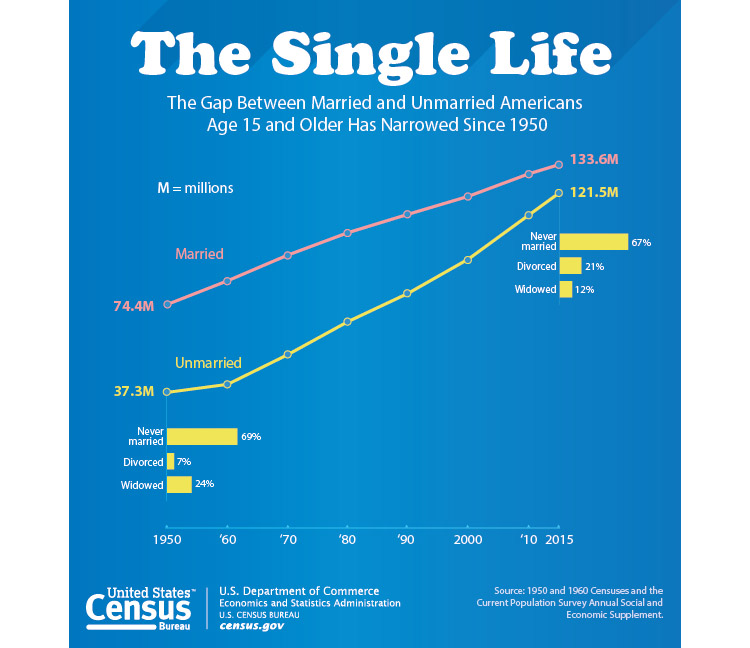

The population gap between married and unmarried Americans has contracted sharply over the past 65 years.

Head Solutions Group conducted an online survey for TD Ameritrade in mid-August with 2,019 Americans aged 37 and older, including 1,011 married individuals, 496 who were single and never married and 308 who were divorced.

Married individuals in the study reported annual personal income of $61,700, $13,100 more than widows/widowers reported and $9,800 more than divorcees.

“Advance planning could provide a much-needed boost in financial security for those who unexpectedly end up alone at any phase of their lives,” David Lynch, managing director and head of branches for TD Ameritrade, said in a statement.

“Considering divorce or the loss of a spouse is a smart addition to any long-term financial plan. It’s no different than planning for things like a major illness, disability or potential long-term care needs.”

The survey found that widowed and divorced Americans were likelier to trust themselves than to trust a financial advisor to manage their savings and investments.

Advisors face unique challenges in retaining female clients following a divorce or a spouse’s death.

{kind=link}