Podcast Center

Podcast Center Video Center

Video Center Webcasts

Webcasts Resource Center

Resource Center Events

Events

June 24, 2011 at 11:51 AM

June 24, 2011 at 11:51 AM

The capital markets abhor a vacuum, and as exchange traded funds grow more popular, their uses keep multiplying to fill every space that their creators and investors can identify.

In the world of registered investment advisors, many RIAs are now working with ETF firms to create custom-made funds to suit their clients’ portfolios.

For exa mple, New York-based ETF firm IndexIQ routinely consults with registered investment advisors about what they’re looking for, “where their pain points are” and problems with existing products in the marketplace, says CEO Adam Patti (left). And after doing the market research, IndexIQ custom-designs products capable of making Savile Row’s bespoke tailors turn green with envy.

mple, New York-based ETF firm IndexIQ routinely consults with registered investment advisors about what they’re looking for, “where their pain points are” and problems with existing products in the marketplace, says CEO Adam Patti (left). And after doing the market research, IndexIQ custom-designs products capable of making Savile Row’s bespoke tailors turn green with envy.

“We talk to many clients who say, ‘You should launch an ETF based on this.’ Then we’ll compile that data and bring out a product,” Patti said in an interview on June 20. “Over the past couple of weeks, we have launched a Japan mid-cap product and a small-cap real estate investment trust product. Those were directly because of the conversations we’ve had in the field.”

Sometimes the ETFs that get created as a result of those conversations are relatively simple “pure play” creations focused on a single market niche, such as the aforementioned IQ U.S. Real Estate Small Cap ETF, which goes under the ticker symbol ROOF.

Sometimes the ETFs that get created as a result of those conversations are relatively simple “pure play” creations focused on a single market niche, such as the aforementioned IQ U.S. Real Estate Small Cap ETF, which goes under the ticker symbol ROOF.

But other times, the quants on IndexIQ’s academic board create a more complex set of proprietary investments capable of making hedge fund managers turn red with rage. How? By using a rules-based philosophy that combines the beta benefits of traditional index investing with the high alpha returns sought by active managers.

In short, the firm designs cheap, liquid ETFs suitable for portfolios of any size that replicate the returns of expensive, locked-up hedge funds.

When an RIA recently came to Kevin Malone (left), president of Greenrock Research, which offers asset allocation strategies, Malone recommended an IndexIQ portfolio combining three hedge fund replication ETFs, a mutual fund and an absolute-return, inflation-hedging ETF:

When an RIA recently came to Kevin Malone (left), president of Greenrock Research, which offers asset allocation strategies, Malone recommended an IndexIQ portfolio combining three hedge fund replication ETFs, a mutual fund and an absolute-return, inflation-hedging ETF:

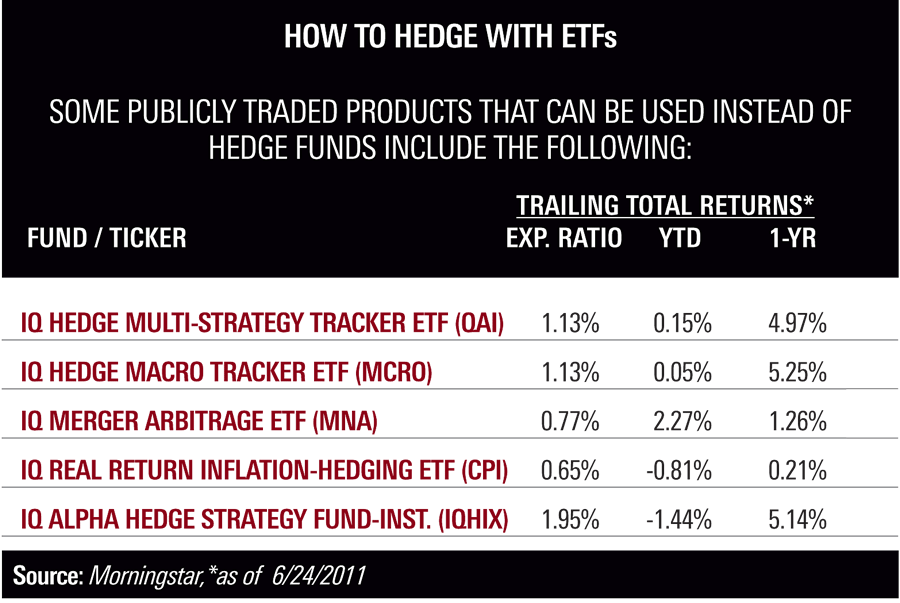

- IQ Hedge Multi-Strategy Tracker ETF (QAI)

- IQ Hedge Macro Tracker ETF (MCRO)

- IQ Merger Arbitrage ETF (MNA)

- IQ Alpha Hedge Strategy Fund mutual fund (IQHIX), which is a mutual fund

- IQ Real Return inflation-hedging ETF (CPI)

“What happened was, the RIA called us and said, ‘George Smith has $50 million, and these are his goals. What should the portfolio look like?’ We worked collaboratively to come up with the asset allocation strategy,” Malone recalled. “When we got to alternatives, we said, ‘This should be half of your alternative

allocation, these IndexIQ ETFs.’ Then two months later, the same client called and said, ‘We’ve got this $100,000 portfolio. We used the same solution.’ That’s the brilliance of it—it’s not just the solution for a small client. It’s the solution because it has intellectual integrity. This is a great idea for anybody of any size.”

Malone pointed to Roger Ibbotson and Peng Chen’s 2011 study, “The ABCs of Hedge Funds: Alphas, Betas, and Costs” (Chen was president of Ibbotson Associates when Ibbotson sold the firm to Morningstar in 2006) which concludes that hedge funds between 1995 and 2009 have resulted in about 10% to 15% of alpha return, 60% to 65% of beta return and 20% to 25% in fees.

“Why would you pay hedge fund fees where you’re only getting alpha return that’s 10% to 15%? We think we have fee structures that are about a third or a quarter of what hedge funds are by using ETFs, and we’re probably going to get similar returns and have complete liquidity. That’s what we use IndexIQ for,” Malone said. “We could take our clients’ money out of those ETFs tomorrow. That’s why we are perfectly happy with beta. We can get beta as the core, like you would with an alternative investment fund of funds, and we can do it for a third or a quarter of the cost and have liquidity.”

The five IndexIQ funds achieve a similar return pattern to a hedge fund over approximately 18 months, Malone said.